The Future of Bill Payments: Request-to-Pay at Scale

The Future of Bill Payments: Request-to-Pay at Scale

Bill payments have long been plagued by inefficiencies—late fees, reconciliation headaches, and poor customer visibility. This blog explores how R2P at scale is redefining bill payments for customers, billers, and financial institutions.

Written By

FT Scholar Desk

SHARE THIS

Unlock exclusive FyscalTech Content & Insights

Subscribe now for best practices, research reports, and more.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Heading 1

Heading 2

Heading 3

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Paying bills is one of the most frequent financial activities in the world, yet for decades it has remained a frustrating and fragmented experience. Most customers still receive bills in static formats whether by post, email, or PDF statements and then must remember to initiate a payment separately. On the other side, billers chase overdue payments, spend heavily on reconciliation, and rely on collections when accounts fall behind. This static process creates friction, generates hidden costs, and erodes trust between customers and service providers.

Request-to-Pay (R2P) offers a very different model. Instead of treating bills as one-way notifications, R2P creates a two-way, interactive request that flows over real-time payment rails. The biller sends a structured digital request, and the customer can immediately approve, decline, or schedule the payment within their trusted banking or payments app. This shift turns the bill from a passive document into a dynamic interaction. At scale, it promises to transform how recurring payments are managed across industries and geographies.

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Type image caption here (optional)

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

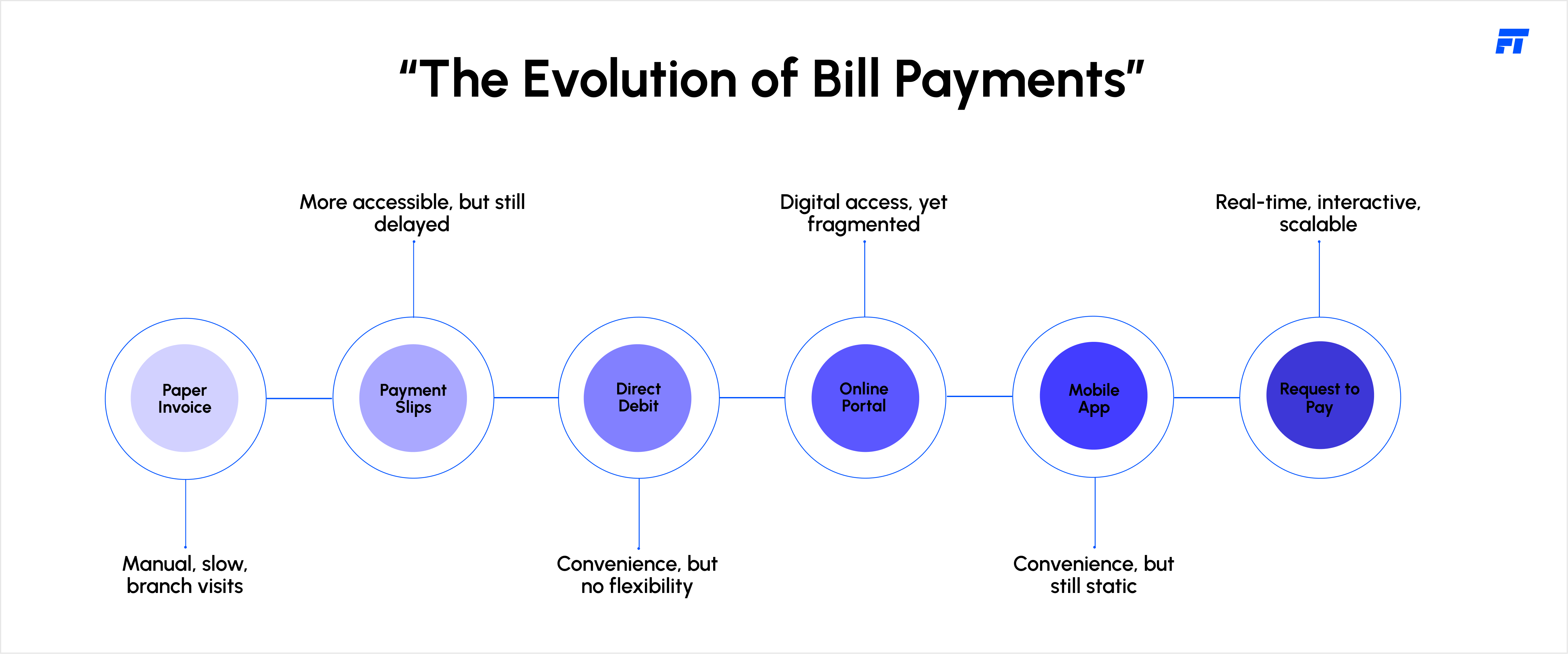

Bill payments have been part of daily financial life for centuries. From the earliest days of utility companies mailing paper invoices to households, customers have been expected to track due dates, write cheques, and often physically visit branches to settle accounts. By the mid-20th century, payment slips and postal orders made the process somewhat easier, but it still relied heavily on manual effort and delayed settlement.

The arrival of direct debits and standing instructions in the 1980s and 1990s was a milestone. Customers could finally automate recurring payments for utilities, mortgages, or subscriptions. While efficient for billers, this model locked customers into rigid schedules and gave them little control once instructions were set up.

The digital age introduced online portals and mobile apps, which made bill payments more convenient. Customers could now log in, enter details, and pay instantly. Yet the fundamental model remained the same: the bill was a static document, and the payment was a separate manual step.

Bill Payments in Today’s World

In today’s hyper-digital economy, the traditional bill payment process feels outdated. Customers receive bills scattered across multiple channels emails, SMS alerts, postal letters, and PDF attachments and must manually track, remember, and pay each one. Even when customers set up auto-debits, they often lose visibility and flexibility.

On the other side, billers face a different set of challenges. Payments may arrive late or incomplete, reconciliation becomes resource-intensive, and collections efforts consume time and money. The system is inefficient, costly, and increasingly misaligned with how customers expect financial services to work in a real-time, mobile-first world.

This misalignment is magnified by broader shifts in payments. With real-time rails like UPI in India, SEPA Instant in Europe, and RTP in the US, customers are accustomed to instant transfers and real-time balance updates. Waiting days for a bill to be processed or seeing balances update only after clearing cycles feels archaic.

Why Traditional Bill Payments Fall Short

Despite a decade of digitisation, most bill payment experiences still mirror legacy paper processes. Customers receive bills scattered across multiple channels some in the mail, some via email, some hidden in provider portals making it difficult to track obligations in one place. Even when customers pay online, the payment itself often relies on manual entry of reference numbers or account codes, increasing the risk of errors. For billers, this fragmented process translates into reconciliation headaches. Payments arrive without the right metadata, forcing teams to spend hours matching them manually against outstanding invoices.

Traditional systems also offer customers very little flexibility. Once a bill is issued, there are few options to negotiate a change, request an extension, or break it into partial payments without escalating through call centers. And because the system is based on static invoices, failure rates are high: mistyped payment details, overlooked due dates, and disconnected reminders all contribute to late or missed payments. For both sides, the result is inefficiency, frustration, and financial risk.

The Shift: Request-to-Pay at Scale

Request-to-Pay reimagines this process by embedding interactivity and real-time capability at its core. Rather than sending a statement and waiting passively, a biller sends a digital request directly to the customer’s banking app. The customer can then respond in real time choosing to pay immediately, schedule for later, or even query the bill if something looks incorrect. This creates a live exchange instead of a one-directional notification.

At scale, the implications are significant. Customers gain confidence and control, knowing that bills arrive in one trusted place and that they can act on them with a single tap. Billers gain faster settlement and improved cash flow, as real-time requests reduce the lag between billing and collection. Banks, meanwhile, position themselves at the center of this interaction, offering value-added services and creating new opportunities to innovate around customer engagement.

Importantly, R2P also aligns with the global rollout of real-time payment infrastructures. Initiatives like SEPA Request-to-Pay in Europe, UPI in India, and the RTP network in the United States show that the rails for this transformation are already being built. The challenge ahead is not feasibility, but scale.

Strategic Advantages of Request-to-Pay

The adoption of R2P delivers a cascade of benefits for all parties involved. For billers, the ability to send real-time requests directly into customers’ trusted apps means faster payments, fewer defaults, and better predictability of cash flows. ACI Worldwide reports that organisations using real-time collection methods see up to a 20% improvement in cash flow forecasting accuracy.

For customers, the experience shifts from stressful to seamless. Instead of tracking due dates across emails and portals, they receive timely requests in one channel and can act on them with confidence. The risk of late fees diminishes, and transparency improves significantly.

Improved Cash Flow for Billers: Enables faster settlements, improving cash flow predictability by up to 20%.

Customer-Centric Experiences: Delivers interactive, trusted payment requests that reduce friction and boost loyalty.

Reduced Cost-to-Serve: Automates reconciliation, cutting manual effort and freeing finance teams for higher-value tasks.

Greater Financial Inclusion: Provides underbanked users with a simple, secure way to manage payments via mobile.

Ecosystem Innovation: Lets banks and fintechs integrate R2P with tools like budgeting, PFM, or BNPL solutions.

The Road Ahead: From Pilots to Scale

Although R2P pilots have launched in many markets, true scale will require alignment across several dimensions. Standardisation is essential, so that requests are interoperable across banks and regions. Frameworks such as SEPA’s Request-to-Pay initiative and the adoption of ISO 20022 messaging standards are important steps toward harmonisation. Widespread bank participation will also be critical R2P cannot succeed if customers and billers only see patchy coverage. Education and adoption campaigns will be equally important to help customers understand why this new approach is superior to the old reminder-based model.

Looking further ahead, the potential for cross-border R2P is especially exciting. As global payment infrastructures become more connected, the idea of paying an international utility bill, tuition invoice, or subscription service via a standardised R2P request could move from vision to reality. The Bank for International Settlements (BIS) has already highlighted the role of interoperable, event-driven infrastructures in shaping the future of payments, and R2P is a clear example of that principle in action.

If you’re exploring how Request-to-Pay could fit into your payment strategy, our experts at Fyscal Technologies can help you assess the opportunities, challenges, and implementation pathways.

.svg)

.png)

.svg)

.svg)

.svg)